Malaysia: +603 2779 0098

There has clearly been a surge in interest for digital pathology adoption over the last two years.

Imogen Fitt of Signify Research attended the 8th Digital Pathology and AI Congress: Europe at the London Heathrow Marriott Hotel. In the article below she shares her thoughts on the conference and overall outlook for the future of the digital pathology market.

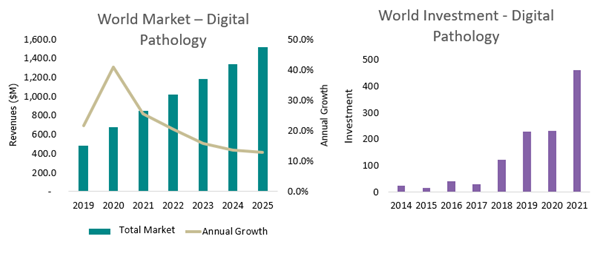

Thanks to the priority placed on remote workflows during the COVID-19 pandemic, hardware and platform software vendors benefited greatly from increased sales during 2020 and 2021. Similarly, AI algorithm developers also saw increased interest, and although clinical adoption did not yet begin in earnest, 2021 saw investment for these companies more than double.

Figure 1: World Market Revenues & Investment for the Digital Pathology Market

Lack of Forethought for the Future, Leads to Huge Costs Later On

Whilst this rapid surge in interest is certainly welcomed, conversations with stakeholders in the field have revealed several market challenges yet to be fully addressed.

Some of these centres around quality control and intra-disciplinary standards that can be addressed solely by pathology bodies; however, increasing care must also be paid towards the role of digital pathology in the context of the wider healthcare ecosystem.

If the history of digitisation in other markets (such as radiology and EHR) tells us anything, it’s that rapid adoption without careful consideration of future needs can quickly hinder overall progress in treatments. Healthcare is quickly evolving towards a focus on ‘personalised medicine’, which involves embracing newer technologies and creating interdisciplinary workflows.

Whilst pathology currently exists relatively siloed from other healthcare departments, tumour boards and other practices such as clinical trial recruitment and life sciences research will increasingly require further input from these sources of data.

Therefore, when approaching digital pathology adoption providers must also carefully consider the trends of the next few years, and whether they wish to place priority on facilitating these improvements.

With that in mind, below we explore some of the issues yet to be fully addressed by the digital pathology market and discuss how these might change over the short-long term.

Image Viewing Standardisation: Hardware

Scanner hardware has developed significantly over the last decade to provide several functions according to individual lab requirements. Providers now have access to scanners able to process anything from 1 to 400+ slides at a time, as well as scanners that are equipped for advanced imaging techniques like immuno or fluorescent staining.

However, some believe there is yet more progress required. Pathology, unlikely radiology, is a discipline reliant on analyses of colour, which is integral to the identification of specific tissues and cells. However, studies have shown that there is a significant variance in the colour profiles produced by and between these scanners. [1] Scanners on the market today each use different image processing algorithms which can result in variations in colour contrast and intensities. It is perhaps counterintuitive then, that there exist no global standards for colour despite calls for such measure amongst professionals.

The requirements for the display and review of digital pathology images also remain unregulated. Indeed, whilst other specialities like mammography have displays stringently regulated by the FDA, no such requirement yet exists for digital pathology.

This may come as a shock to many who have a passing interest in the market. Indeed, most would be wrong persuaded that, at least in the case of the US market, there was a significant case of ‘overregulation’ which inhibited progress in the market. This case was made clear when the first two FDA approvals for a digital pathology product consisted of end-to-end imaging pipelines involving proprietary data formats and components. These were offered approval only in 2017 and 2019 respectively, with subsequent approvals for what could be considered separate products (hardware/software) also requiring a ‘one-system’ approach.

When the FDA relaxed these regulations in April 2020 to support healthcare providers dealing with COVID-19, the adoption of new entrants soared. It could therefore be argued that the regulatory authorities are perhaps focusing too much on overregulating ‘closed’ looped systems and not enough on adjacent market components.

Vendors themselves are aware of pitfalls in viewing standards, with leading display company Barco already having filed for and advertising FDA approval for its 8MP MDPC-8127 display. However, it should be noted by providers that this approval hinges on the device’s substantially equivalent nature to legally marketed predicate devices and not on it’s applicability for use in digital pathology. As yet no consensus on the resolution required for primary or secondary review is enforced.

FFEI, a UK-based digital imaging solutions provider, is addressing a different pitfall in seeking to tackle colour fidelity with its Sierra portfolio, which enables the production of a DICOM compliant ICC profile used to calibrate colour and account for distortions.

Ultimately though, we at Signify Research remain sceptical in both these approaches. Until both initiatives receive regulatory backing in the form of guidance or requirements from substantive bodies, we find it likely that in the near term the case for added purchase of these best-of-breed solutions may fall to the wayside.

Initial costs for digitisation in the market remain a significant barrier for providers, with high throughput scanners selling at an average of $237.2k USD worldwide in 2020. Approaches in the near term may then be best directed at developing indirect sales channels through scanner and software vendors who are more easily placed to market the products as an ‘accessory’.

Software Implementations and the Need for More Storage

It’s not just accessory components that are in danger of being overlooked, however. Increasingly, it’s becoming apparent that providers need to think about the long-term impacts of digitisation and plan for technical IT requirements that are associated with image storage.

There are two deployments associated with this.

On-premises deployment, which houses the data locally on a provider’s own servers is the traditional approach for most broader diagnostic software. Because of this, pathology departments see this method as an increasingly attractive way to leverage already-existing capital investments in IT infrastructure, networking, and cybersecurity.

However, there remains a significant problem with this approach which pathology is set to experience much more quickly than its peers. Pathology images are typically magnitudes larger in file size than radiology’s counterparts and therefore as pathology departments scale their digital pathology use the use of these servers, and consequential need to invest in further costs, scales quickly.

For this reason, the use of cloud-based deployment models is now being offered with some newer digital pathology platforms. These cloud implementations are made more attractive as they often come with the option for operation billing models. However, this deployment model also comes with its own nuances. When considering adoption, providers are cautioned to consider their own local network infrastructure capabilities to ensure exchange and thus performance is not affected, particularly if personnel require access to large volumes of 5GB+ images daily.

The consensus from vendors indicated that the preferred method of deployment combines the best of both these approaches. By adopting a hybrid model, providers can store newly acquired images short-term on-premises, and after review and diagnosis can then shift these to longer-term ‘cold’ storage in the cloud. By doing so providers are then able to avoid mounting costs whilst also not compromising on performance.

However, whilst this approach is clear to the vendors associated with the market, the need for investment in educating providers themselves is still a significant issue affecting implementations today. Clearer guidance is required needed to help providers make these decisions, likely in the form of case studies and proactive initiatives.

The Future Requirement for Interoperability

Looking further into the future regarding the changes that will eventually be required by digital pathology departments, it’s clear that broader changes to care models, including multidisciplinary collaboration, are soon going to require higher availability of pathology content across healthcare enterprises.

Yet today the digital pathology market has yet to adopt a singular standard format. Whilst many proprietary formats do exist, the market has yet to reach a consensus that will enable it to move forward.

Arguments have been put forward for the DICOM-based approach, and it’s likely that the rise of enterprise imaging will help to facilitate this, particularly in Europe, over the next few months. However, for academic and research users, research-level DICOM standards which suit multiplexed imaging and single-cell profiling are still some way off.

The market will need to decide soon, however. This comes as increasing funding for computation pathology algorithms is driving focus on the need for adequate data aggregation and digitalisation of archives. If pathology truly wants to make use of the reported advantages associated with AI adoption, it will require more focus on creating greater datasets for algorithm training.

The Next Steps Will be Integral for the Future of Pathology

Whilst other barriers remain to digital pathology adoption, such as workforce hesitancy and significant upfront costs, there is encouraging evidence that vendors are beginning to meet these challenges head-on and make progress. The market for digital pathology is expected to grow well past 2025, and although Europe initially lagged behind the US market’s growth in 2020, the future remains bright.

But this is no time to rest on one’s laurels and wait for the opportunity to present itself. Now especially, the digital pathology market must look forward and use expected future developments to guide today’s decisions.

This article was first published by Signify Research on 11th January 2022. It is reproduced by kind permission.

![]()

[1] Rajaganesan S, Kumar R, Rao V, et al. Comparative Assessment of Digital Pathology Systems for Primary Diagnosis. J Pathol Inform. 2021;12:25. Published 2021 Jun 9. doi:10.4103/jpi.jpi_94_20

Only products with same currency can be added to the basket. Clear the basket or finish the order, before adding products with another currency to the basket.